Definition of blockchain

- 1555

- 0

- 0

What's a blockchain?

Blockchains are databases for recording and storing information related to transactions. The databases gather all the transactions carried out since the creation of the blockchain. The information is stored in the form of a block, containing several transactions, made during a given period. All its blocks together form a blockchain.

Source: Blockchain France

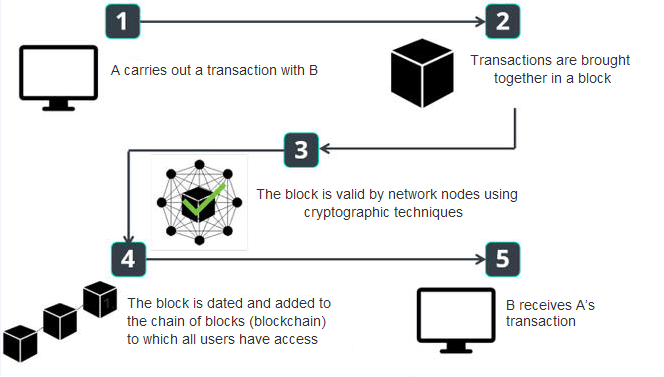

The major difference form current technologies is that transaction verification is decentralized. Each party confirms the transaction and, once this operation is completed, the transaction is verified then encrypted to be integrated into the blockchain. The encryption is performed by a node that can be a person (called a miner in the jargon) or by a trusted third party (an institution) depending on the type of blockchain. Effectively, blockchains can be public or private. Here is a chart summarizing the operation of a Blockchain:

The advantages of blockchain technology

- Safety: Once a transaction has been recorded in a blockchain, it cannot be changed. Current technologies do not guarantee this data inviolability.

- Accessibility: Operations recorded in blockchains are visible by everyone, if they are public. All participants then have access to the database confirming the transactions. There is total transparency.

- Reduced costs: Blockchains make it possible to eliminate a large number of intermediaries. The only intermediary between 2 economic agents passing a transaction is the encrypter (a person or an entity). Fewer intermediaries means lower operating costs compared to other technologies.

The different blockchain models

Public Blockchains

The transaction databases are public, open to everyone. There is total transparency. Each person can freely make a transaction at any time. Verification and integration of transactions into blockchains are carried out by natural people called miners. These miners are geeks, equipped with powerful computer systems which encrypt data.

There are thousands of miners in the world and they are paid for each encryption operation of a block. Only the fastest are paid. With public blockchains, there are therefore no trusted intermediaries in the process and there is total decentralization. The database is shared by its different users, without intermediaries, which enables everyone to check the validity of the chain. It is the most well-known model, it is used in particular by Bitcoin.

Consortium blockchains

Unlike the public blockchain, data verification and encryption is not performed by a natural person but by several trusted third parties. These trusted third parties may be, for example, a financial institution. This model is therefore only partially decentralized. The trusted third parties decide who has access to the database. Otherwise, access is restricted to participants in the blockchain. For example, a consortium blockchain could be set up between banks to have a common database of all interbank transactions.

Private Blockchains

This is a centralized model. Data recording and encryption are performed by a single entity. This entity must be considered as a trusted third party. Access to blockchains can be open to all or restricted to participants (the 2nd option is the one most often chosen). This model is of particular interest to private companies.

Open source technology

Blockchain is an open source model, i.e. its code is freely available and accessible to everyone. Blockchain technology doesn't belong to anyone. Any individual or entity can use a blockchain as they wish. In a public model such as Bitcoin, there is total transparency. Other cryptocurrencies, competitors of Bitcoin, were created later using the same code.

Public blockchains based on the community wide model are not adapted to the needs of companies and they mainly use private blockchains. In the case of Bitcoin, a transaction has no legal value, it is a simple OTC contract.

Private blockchains make it possible to define a legal framework, given that the operation passes through a trusted third party. Moreover, in-house developments, for adapting a blockchain to an activity, are not in the public domain. These developments are only accessible to the developer and not for all the participants of the blockchain. It is for these reasons that private blockchains are the most popular with companies.

Consortium blockchains are based on the same principle but their use is problematic. Effectively, although there are numerous advantages, all trusted third parties (nodes) have access to the blockchain data. However, there is data that must not be shared between third parties. To date, there is no legal framework to address this problem.

A revolutionary concept

For the moment, blockchain technology is used very little but this could change rapidly in the coming years. Many current economic models would be challenged. Compared to current economic models, blockchains offer flawless security, increased transparency and simplified and less costly management of operations (reduction in the number of intermediaries).

Many governments, institutions and companies are currently studying how to adapt the blockchain principle to their area of competence. Because of their network operation, blockchains could make it possible to eliminate all regulatory authorities. There are 3 large, distinguishable fields of application:

- Transfer of assets: Transferring the ownership of an asset (financial, real estate, etc.) could be done via a blockchain. For example, imagine a world without notaries. Transactions would be recorded directly via an open land registry (public blockchain).

- Traceability: Knowing the origin of a product or an asset could be done via a blockchain. Imagine a world where we know the origin of each component of a product, the complete history of an asset.

- Smart application: Concluding OTC contracts and ensuring the execution of terms and conditions could be done via a blockchain. Imagine a world without bailiffs, insurers, bankers, AirBnb, Uber, Ebay, etc.

A threat to employment

Blockchain technology is revolutionary and can be applied to almost any field of activity. The problem is that this technology puts many jobs at risk by making a lot of professions unnecessary.

In the banking sector alone, Citigroup has estimated that 2 million jobs could disappear in European and American banks in the next 10 years due to the use of blockchains and new financial technologies.

It is hard to see companies depriving themselves of blockchains in view of the savings they could bring them. In the coming years, the global economy could change dramatically. The only barrier remains to define a legal framework for each field of activity. Developing the technology is not the longest step.

On the other hand, at the administrative level, adopting blockchain technology could take much longer. Although most administrative services can be eliminated, governments will not want to be held responsible for a sharp rise in unemployment due to a political decision. The transition will therefore take longer than in the private sector, but in view of the operating savings that this can generate, there is no doubt that it will happen one day.

The revolution has arrived!